Business

Doing business in China is growing tougher, more uncertain, says European business group

Doing business in China is growing tougher, more uncertain, says European business group

Uncertainty and “draconian regulations” have drastically raised risks for foreign businesses in China, a report by a European business group said Wednesday.

The lengthy paper by the European Union Chamber of Commerce in China urges China’s leaders to do more to address concerns that it says have “grown exponentially” in recent years.

“This report comes at a time when the global business environment is becoming increasingly politicized, and companies are having to make some very tough decisions about how, or in some cases if, they can continue to engage with the Chinese market,” it says.

The study, compiled by the chamber and the China Macro Group consultancy, echoes concerns that have been raised by European and American companies operating in China. Foreign investment fell 8% last year from a year earlier as companies recalibrated their commitments in the world’s second largest economy.

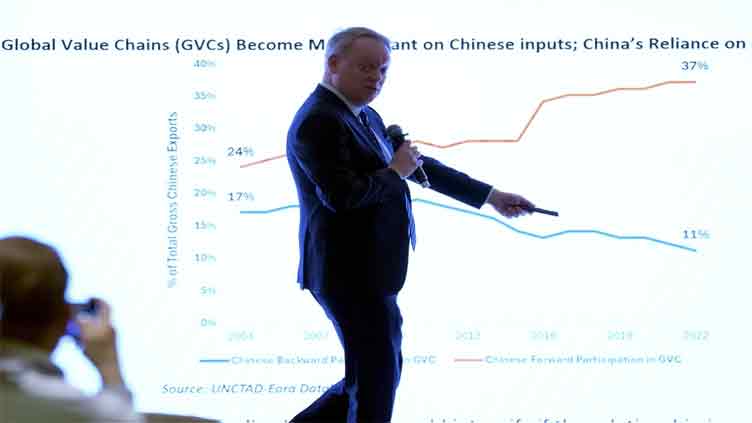

EU Chamber officials said China’s changing business environment partly reflects moves by Beijing to minimize risks due to trade friction and dependence on imports of key commodities or industrial products. That’s especially the case given trade friction with Washington and discussions about “decoupling” supply chains from China after the disruptions that occurred during the COVID-19 pandemic.

But they said European companies also must manage their own risks.

China has sought to emphasize its openness to foreign companies and investment. Its commerce ministry spokesperson said the country was working to ensure 100% access to manufacturing by eliminating remaining trade barriers.

On Tuesday, the State Council, China’s Cabinet, issued an updated version of an action plan announced in July to promote more foreign investment, especially in high-tech areas favoured for growth such as computer chips, biopharmaceuticals and advanced equipment. It promised tariff exemptions and called for stopping practices that discriminate against foreign companies.

But other actions have run counter to that spirit of openness. Raids on foreign businesses in China, unclear state secrets laws and tightening rules on handling of data have generated unease among many foreign business people in the country.

“The number and severity of risks companies find themselves having to navigate has grown exponentially in recent years,” Jens Eskelund, president of the European Chamber in China, told reporters in a briefing before the report’s release.

At the same time, Beijing has not addressed many of the issues raised by foreign businesses, among them access to government procurement contracts, which are vital given the huge role of state-owned companies in the economy.

It’s particularly difficult for medical equipment companies and research and development. Meanwhile, pharmaceutical companies are “quite alarmed by data security regulations that make clinical trials impossible,” said Markus Herrmann Chen, co-founder and managing director of the China Macro Group.

“We are still the odd guys out, and this needs to change,” Herrmann Chen said.

Part of the challenge results from China’s increased focus on national security in terms of reliance on technologies vital to its own industries. In part, such strategies are driven by U.S. moves to cut off business with Huawei Technologies and to prevent sales of leading edge computer chips and the equipment needed to make them.

American companies have expressed similar concerns. Sean Stein, the chair of the American Chamber of Commerce in China, said recently that China has made progress in addressing some issues but not others.

“The business community would like both sides to be much clearer about the definitions of national security and how it’s determined,” he said in an interview before an annual chamber banquet with Chinese officials. “Because what we need is … predictability, and we need certainty.”

One sore point for European business: a Chinese announcement of plans for anti-dumping investigations into three French brandy producers: E Remy Martin & Co, Martell & Co and Societe Jas Hennessy & Co.

“It’s hard to see how 300 euro ($330) bottles of XO can be accused of dumping,” Eskelund said.

For its part, China is unhappy with an ongoing European Union investigation into subsidies for electric vehicles in China and whether they have given Chinese makers an unfair advantage in European markets.

Meanwhile, with regard to cybersecurity, Eskelund said “we’ve seen some very draconian new regulations being published in China.”

He said Europe’s approach to trade and investment issues was “targeted, very limited and very focused on eliminating ‘critical dependencies,’” not at competing with China. But companies still must hedge against risks or potentially be blindsided by policy shifts.

At the same time, companies also face risks in cutting back and must bring their “best game” to China, while others feel too exposed, especially after the shocks of the pandemic, when entire cities were ordered into lockdown and factories suspended production at times.

China’s market has become “less predictable, reliable and efficient,” the report says, partly because the business environment is more politicized.

Eskelund called on China to restore predictability to the regulatory environment.

“Predictability was one of the main things that made China so enormously attractive,” he said. “We might not like everything we saw but we knew what we got.”

He said the purpose of the report is to try to bring the debate over de-risking and national security down to the level of specific industries and commodities so that the various sides are not just hurling big abstract concepts at each other.

“We want to find common ground,” he said. “We want to work with China on these issues. We want to work with Europe on these issues.”

The dollar steadied against major peers on Thursday, continuing its near paralysis of the past two days before more concrete announcements on tariffs from U.S. President Donald Trump.

A spate of central bank policy decisions are also due over the next week, with the Bank of Japan widely expected to raise interest rates at the end of a two-day meeting on Friday.

Rate decisions from the U.S. Federal Reserve and European Central Bank are scheduled for Wednesday and Thursday of next week, respectively.

The dollar index – which measures the currency versus six top rivals, including the euro and yen – was flat at 108.25, following two days of gains of around 0.1%.

On Monday, it tumbled 1.2%, its steepest one-day slide since November 2023, as Trump’s first day in office brought a barrage of executive orders, but none on tariffs.

So far this week, Trump has mooted levies of around 25% on Canada and Mexico and 10% on China from Feb. 1. He also promised duties on European imports, without giving details.

“President Trump has so far taken a less hostile-than-expected approach to China,” amid overall “softer-than-expected policies and tone on tariffs”, said Carol Kong, a currency strategist at Commonwealth Bank of Australia.

At the same time, “we are cautious (that) risk sentiment remains fragile and can quickly turn sour if President Trump strikes a more aggressive tone.”

The Chinese yuan was little changed at 7.2812 per dollar in offshore trading .

Wall Street’s main indexes rose Wednesday, with the S&P 500 hitting an intraday record high thanks to strong Netflix earnings and a rally in tech shares.

Japan’s yen edged up about 0.1% to 156.40 with markets pricing 95% odds of a quarter-point hike on Friday.

The euro was flat at $1.0411. The ECB is widely expected to cut rates by a quarter point next week.

The Canadian dollar held steady at C$1.4386 against the greenback. The Bank of Canada is seen as likely to reduce rates by a quarter point next Wednesday.

The Mexican peso was little changed at 20.47 versus the U.S. currency.

Oil prices dipped in early trade on Thursday, extending losses amid uncertainty over how proposed tariffs by U.S. President Donald Trump on several countries would impact global economic growth and energy demand.

Brent crude futures fell 23 cents, or 0.3%, to $78.79 a barrel at 0135 GMT, while U.S. West Texas Intermediate crude (WTI) eased 18 cents, or 0.2%, to $75.26.

In its previous session, Brent futures settled at $79.00 in a fifth straight day of losses. WTI futures settled at $75.44 in a fourth consecutive day of declines.

Trump has said he would add new tariffs to his sanctions threat against Russia if the country does not make a deal to end its war in Ukraine. He added these could be applied to “other participating countries” as well.

He also vowed to hit the European Union with tariffs, impose 25% tariffs against Canada and Mexico, and said his administration was discussing a 10% punitive duty on China because fentanyl is being sent to the U.S. from there.

Meanwhile, estimates from an extended Reuters poll showed that on average U.S. crude oil stockpiles were expected to have fallen by 1.6 million barrels in the week to Jan. 17.

Gasoline stockpiles were estimated to have risen by 2.3 million barrels last week, and distillate inventories were likely to have gained 300,000 barrels.

The poll was conducted ahead of the American Petroleum Institute industry group’s report and another from the Energy Information Administration at 12:00 p.m. ET (1700 GMT) on Thursday.

European wind shares fell on Tuesday (January 21).

The reports were delayed by a day due to the Martin Luther King Jr. Day federal holiday on Monday.

Pakistan and Saudi Arabia have reaffirmed their commitment to further strengthening the bilateral economic ties for shared prosperity.

The commitment was expressed when Finance Minister Muhammad Aurangzeb met with his Saudi counterpart Mohammad bin Abdullah Al-Jadaan on the sidelines of World Economic Forum Annual Meeting in Davos.

Muhammad Aurangzeb highlighted the key reform measures undertaken by the Government to promote economic stability and sustainable growth.

He briefed him on structural reforms, fiscal discipline and regulatory improvements that have contributed to an improved investment climate in Pakistan.

Earlier, Aurangzeb met Anna Bjerde, Managing Director of Operations at the World Bank.

They discussed cooperation between Pakistan and the World Bank, with a particular focus on Pakistan’s macroeconomic stability.

The finance minister emphasized the government’s strong partnership with the Bank and expressed hope that the World Bank would continue playing a key role in the country’s socio-economic development.

OpenAI, SoftBank each commit 19bn dollars to Stargate AI data center

Taiwan’s HTC to sell part of XR unit to Google for 250mn dollars

Microsoft’s LinkedIn sued for disclosing customer information to train AI models

-

Business2 months ago

Business2 months agoAuto industry’s shift toward EVs is expected to go on despite Trump threat to kill tax credits

-

Entertainment3 months ago

Entertainment3 months agoBeyoncé leads the 2025 Grammy noms, becoming the most nominated artist in the show’s history

-

Business3 months ago

Business3 months agoWall Street cruises toward the close of its best week in a year

-

pakistan3 months ago

pakistan3 months agoPM Shehbaz terms promotion of foreign investment as top priority

-

World2 months ago

World2 months agoSix Israeli troops killed, deadly strikes in Lebanon

-

Entertainment3 months ago

Entertainment3 months agoMovie Review: ‘Red One’ tries to supersize the Christmas movie

-

Sports1 month ago

Sports1 month agoSouthampton set to sign Juric as new manager

-

Business2 months ago

Business2 months agoWall Street gains ground as it notches a winning week and another Dow record